Introduction

Since 2010 when financial markets first realised Greece could never afford to pay its debt, the country has been subjected to a brutal regime of austerity. The economy has collapsed by 25%,unemployment is 27% (up from 8% before the crisis began) with youth unemployment of 50% andone-in-five now live in severe poverty. Eurozone governments, the European Central Bank (ECB) and International Monetary Fund (IMF) have lent more money which has been used to repay original reckless lenders rather than going into the Greek economy. Meanwhile, Greece’s overall debt has increased as its economy has stagnated because of the punishing austerity measures imposed as a condition of the loans.

Throughout this crisis Jubilee Debt Campaign has warned that the bail-out programme was repeating the disastrous policies forced on developing countries in the 1980s and 1990s. Bailing out European banks rather than making them cancel debts would ensure the private speculators and reckless lenders would get repaid, whilst the public would pay the costs of having to cancel debts in the future. Austerity would crash the economy, increase poverty and unemployment, and increase the relative size of the debt. This is exactly what has happened.

The crashing of the Greek economy and continual increase in debt as a result of bailouts and austerity was foreseen within the institutions conducting the bailout. Leaked minutes of the IMF Board meeting in 2010 which decided on the first bailout showed that many countries were opposed to that approach and thought debts should be cancelled instead.

Most strikingly, drawing on their own experience of failed bailouts in the late 1990s and early 2000s, Argentina argued that a “debt restructuring should have been on the table”.

Brazil said the IMF loans “may be seen not as a rescue of Greece, which will have to undergo a wrenching adjustment, but as a bailout of Greece’s private debt holders, mainly European financial institutions”. India warned that the scale of cuts would start a spiral of falling unemployment which would reduce government revenue, causing the debt to increase, and making a future debt restructuring inevitable.

The debt crisis which affected many developing countries in Africa, Asia and Latin America in the 1980s and 1990s continued for over 20 years. The austerity regimes imposed by international financial institutions in return for bail-out loans meant that economies stagnated, whilst poverty and debt increased. The crisis only came to an end for some countries when debts were cancelled[1], countries defaulted[2], or they benefitted from an increase in global commodity prices. For people in countries such as Jamaica and El Salvador, which did not benefit from any of these, the crisis continues to this day.

This briefing provides an update on the situation in Greece following the agreements in July and August 2015 for Eurozone governments to lend more money – which will primarily be used for debt payments – whilst even more austerity and privatisation conditions are forced on Greece.

Meanwhile, the Eurozone’s proposals for extending the duration over which the debt is to be repaid would have no impact on Greece’s debt payments until the 2030s, and would then limit payments to around 37% of government revenue and 33% of exports, higher than virtually any country in the world today. This is ten times more than Germany’s debt payments following the debt cancellation it received in 1953.

Without proper debt cancellation and a reversal of the damaging austerity policies, the people of Greece face many more years and even decades of stagnation, high unemployment, high poverty and increasing debt.

1. The real bailout beneficiaries

Between 2010 and 2014, of the money lent by Eurozone governments, the ECB and IMF to Greece, 92% was spent on debt payments and bank bailouts, leaving less than 10% to be spent by the Greek government. Beneficiaries of these bailout loans included Greek banks, European banks, US banks, and various financial speculators such as hedge funds and vulture funds.

Of the European banks which benefited, those which held the most Greek debt at the start of the bailout programme in 2010 were German banks, followed by French, Cypriot, Belgian and British banks. British banks which were effectively bailed out include RBS, HSBC and Barclays.[3]

The third bailout and austerity programme, agreed in July and August 2015 and running until 2017, follows this pattern. €86 billion is planned to be lent by the European Stability Mechanism[4], a scheme created and backed by Eurozone governments, over three years. How much is disbursed and when will be decided by Eurozone finance ministers. €23 billion was lent in August 2015, leaving a further €63 billion for the future. Of the €23 billion, €13 billion was used to make debt payments, and €10 billion was given to Greek banks to ‘recapitalise’ them.

The €86 billion of loans is being added to by an expected €6 billion received from privatisation of Greek assets between 2015 and 2016 and €2 billion from the Greek government’s own income, which is being specifically earmarked to contribute to these debt payments and bank bailouts. Of this €94 billion in total:

€54 billion will be spent on debt payments by the Greek government

€15 billion will be spent on debt payments that Greece defaulted on in the early summer of 2015, primarily to the IMF, and to increasing the Greek government’s currency reserves

€25 billion will be used for bank recapitalisation (though the most recent estimates by the ECB suggest that this may ‘only’ need to be €14 billion).

So, none of the EU loans over the next three years will be spent by the Greek government within the Greek economy.

2. Interest rates could increase

The new loans have variable maturities so they don’t all come due to be paid in a three-year period. The average maturity of the loans is 32.5 years, which means half is due to be repaid by 2048-2050, and half further into the future.

The interest rate Greece must pay on the loans is not published. It is based on how much it costs the ESM to borrow, plus some add-ons. The cost to the ESM borrowing is in turn determined by how much it costs Eurozone governments to borrow. It is currently thought that the interest rate charged on loans from the ESM is under 2%.

Crucially, the ESM has borrowed not over the maturity with which it is due to be repaid, but has shorter loans as well. This means it needs to refinance itself, which means the interest rate could change substantially in the future, if the cost of Eurozone government borrowing increases.

3. Greece’s debt continues to increase

With the new loans Greek government debt is now projected by the IMF to be 196% of GDP by the end of 2015, €330 billion. By 2020, the IMF predicts debt will still be 183% of GDP (an increase in absolute terms to €367 billion), based on the recession continuing in 2016, then growth of 2.5%-3% from 2017 to 2020. The European Commission predicts that debt will be 175% of GDP by 2020 and 122% by 2030 again based on relatively high economic growth from 2017 on.

Alternatively, as has happened in many countries in the global South in debt crisis, if the Greek economy continues to stagnate, and if Euro inflation remains low, then Greek government debt as a proportion of GDP will continue to increase as more loans will be needed to pay interest as well as principal on debts.

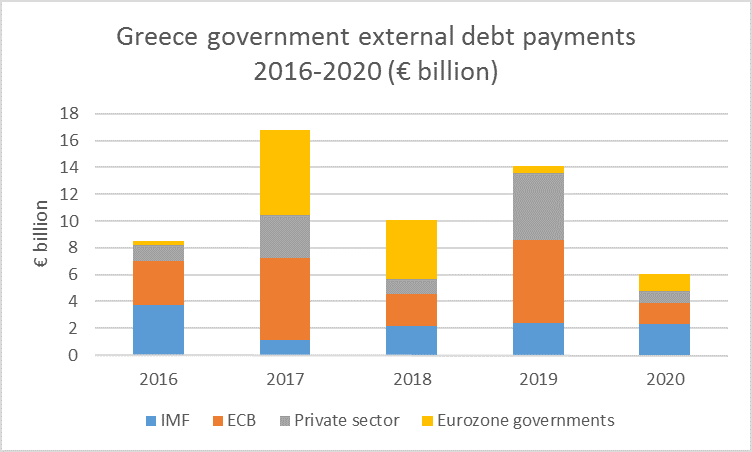

Predicted debt and interest payments from 2016 to 2020 are €55 billion. Of this, €10 billion is interest payments.

4. What debt ‘relief’ is being proposed?

During the summer of 2015, the IMF said that Greece’s debt was unsustainable and that it would not join any new lending programme unless there was a clear commitment to debt relief for Greece. However, it also said this debt relief could come through extending the time over which the debt is paid, rather than reducing the amount. Eurozone governments have refused to negotiate over reducing the total amount of debt owed, but they have indicated debt payments may be moved if Greece implements the economic policies Eurozone governments are demanding (see below).

As part of these debt rescheduling discussions, the IMF has said that Greece’s ‘gross-financing needs’, the amount it needs to borrow to in one year to meet interest, debt principal payments and any remaining deficit, should be capped at 15% of GDP. The European Commission has indicated that that it agrees with this cap, saying this is the level which is sustainable.

At present, Greece’s gross financing needs come entirely from its debt payments (its primary deficit is 0). So the proposed 15% cap is a cap on debt service. 15% of GDP currently amounts to €26 billion, well above the amounts Greece is expected to be paying between 2016 and 2020.The European Commission predicts that debt payments will increase through the 2020s, but that the 15% threshold will only be exceeded after 2030, and that payments could be reduced to below the 15% of GDP threshold by extending maturities on debt payments and interest coming due then. So the proposal for ‘debt relief’ is to not give any for 15 years.

Government debt payments as a proportion of GDP is not the measure usually used to assess debt sustainability levels. For developing countries in debt crisis, the two key measures of debt payments which have been used by the IMF and World Bank are external debt payments as a proportion of government revenue, and external debt payments as a proportion of exports.

Below are the projected external debt payments as a proportion of revenue and exports from 2016 to 2020, based on the IMF predictions for relatively strong growth of government revenue and exports. In 2017, payments go over 20% of revenue and exports, and average 14% of revenue over the five years and 13.2% of exports.

The Eurozone’s proposed upper limit on external debt payments of 15% of GDP would equal 37% of revenue and 33% of exports, higher than virtually any country in the world today.

In contrast, in 1953 Germany had half of its debt cancelled by countries including the US, UK and Greece. The agreement, which came out of comprehensive negotiations on the debt in London, also made debt payments conditional on Germany having a trade surplus with the rest of the world, thereby earning the money to actually be able to repay the debt (rather than needing to borrow or sell assets to do so). The debt relief Germany received in 1953 led to debt payments being limited to 3% of exports, 11 times less than is being proposed for Greece.

Greece has had one previous round of debt relief which actually led to its debt increasing while creating large profits for some vulture funds. In 2012, two years after the bailouts began, it was finally accepted that Greece needed some debts cancelling. An agreement was reached with many private creditors to cancel 50% of the debt owed to them.

However, by this stage, the IMF, EU and ECB had been bailing out these reckless lenders for the previous two years, so many had already been repaid. None of the debts owed to the public institutions were included in the debt reduction.

Moreover, whilst the IMF, EU and ECB debts were excluded, debts owed to Greek banks and financial institutions, including pension funds, were not. The 50% debt reduction would have bankrupted many Greek banks, so the Greek government borrowed more money from the IMF, EU and ECB to bail out the banks. The pension funds which lost large amounts were not refunded.

Finally, whilst a large majority of private creditors agreed to the debt reduction, various vulture funds refused to do so. These speculators bought up Greek debts owed under British law cheaply between 2010 and 2012 and have continued to demand to be paid in full, even though they knew when they bought the debt that Greece could not afford to pay everybody in full.

The total amount of ‘vulture fund’ debt which avoided the agreed restructuring was €6.5 billion. The Greek parliament passed legislation to enforce the agreed debt reduction on all bonds held under Greek law, but the British government refused to do the same. The vulture funds have continued to be paid in full, making a huge profit on the amount they bought the debt for. This was effectively profit being given to the vultures by the IMF, EU and ECB through their loans to Greece, which has left a debt for the Greek people.

One vulture fund which has made a large profit out of Greece and the bailout loans is Dart Management, based in the Cayman Islands and run by US speculator Kenneth Dart. Dart Management is thought to have bought Greek government bonds owed under UK law for around 60% of their face value. In May 2012, Greece made a €436 million payment on such bonds, 90% of which is thought to have gone to Dart. In total, Dart Management’s profit from Greece is likely to be over 60%.

Just like the vulture funds, the ECB bought up Greek government debt whilst it was trading cheaply, but insisted on being repaid in full. It is therefore making a large profit on its buying of Greek bonds each time these debts are repaid. The total profit the ECB will make is acknowledged by them to be at least €10.4 billion, though we have estimated it could be as high as €22 billion.

The IMF was also excluded from the debt cancellation. The IMF’s loans were made directly to Greece, unlike the ECB buying up debts which already existed. However, the IMF has charged interest on those loans at a rate far higher than was needed to cover its costs. We have estimated that over the course of the current IMF loans, the IMF will make a profit of €4.3 billion out of Greece. This profit is put in the IMF’s reserves.

At the end of 2011, before the ‘debt relief’, Greece’s government debt was 170% of GDP. In 2013,the year after, it was 174%. It is now (2015) 196% of GDP and expected by the IMF to increase again to 206% of GDP in 2016.

5. Austerity and privatisation conditions

In the summer of 2015, Greece began defaulting on some of its debts, including to the IMF. In July it would have begun defaulting on loans to the ECB. Eurozone governments told the Greek government that if they defaulted on the ECB loans, they would be kicked out of the Euro. Faced with this unpalatable ‘choice’ Greece accepted taking more loans in order to repay primarily the people who were already owed the money. In return the Greek government was made to sign up to even more austerity and privatisation conditions.

Furthermore, the memorandum says that Greece must “consult and agree” with the European Commission, ECB and IMF on any policies and legislation which could affect the objectives of the bailout before they are finalised.

Firstly, the Eurozone is insisting that Greece should have a budget surplus from 2018 on, not including interest payments, of 3.5% of GDP in the ‘medium-term’. The only rich country which currently has such a sustained surplus is oil-rich Norway. Prior to 2018, the targets for the primary budget surplus are 0.5% in 2016 and 1.75% in 2017.

Many developing countries have been told by the IMF to have large primary surpluses to try to reduce their government debt. For example, Jamaica has had a primary budget surplus every year since at least 1990, which has averaged 7.4% of GDP, more than double that demanded of Greece. This huge austerity forced on Jamaica has meant that the economy has stagnated: it is the same size per person as it was 25 years ago. This in turn means the debt has increased, as new loans have been taken out to make interest payments, just as is being proposed in Greece. In the early 1990s Jamaica’s government debt was just under 100% of GDP. Today it is 125% of GDP, despite 25 years of huge primary budget surpluses.

Secondly, it is likely that many of the spending cuts and tax increases which will be introduced have not been included in the officially released Eurozone conditions on Greece, but are required to meet the budget surplus targets. But many specific measures have been.

In terms of taxation, there are some measures to attempt to tackle tax avoidance, including a condition to introduce a new Criminal Law on tax evasion and fraud. However, most of the tax measures demanded by the Eurozone are based on increasing taxes or widening their scope. Some of these proposals are regressive, others less problematic. They include:

Changes to VAT, such as removing exemptions, including for Greek islands, which increase the tax by 1% of GDP (€2 billion)

Removal of a tax refund on diesel for farmers, and other tax increases for farmers

Introduction of a tax on TV adverts

There are also further significant cuts to spending, in a context where Greece’s government expenditure has already fallen from €128 billion in 2009 to €87 billion in 2015 (32% in absolute terms, 36% taking account of inflation).

Detailed changes to pensions are being made which will cut spending on pensions by 1% of GDP (€2 billion) by 2015. This includes raising the age at which people get access to the means-tested public pension to 67.

The Eurozone is also demanding that a means-tested €5 fee for hospital visits is introduced. This by itself is unlikely to raise much money, but the Eurozone governments specifically state that they want it introduced both to raise money and to reduce demand for health services. Other healthcare changes include limiting “access to the most expensive drugs and procedures”, though the conditions do not specify which drugs and procedures these are.

Another condition is a review of social welfare payments in order to cut welfare spending by 0.5% of GDP (€1 billion), and another is to halve heating oil subsidies.

There is a condition to cut military spending by €100 million in 2015 (0.06% of predicted GDP) and €400 million (0.2% of GDP) in 2016. Greece currently spends 2.2% of GDP on the military, the same as France and the UK, and well down from the 3.2% of GDP spent in 2009.

Thirdly, changes to tax and spending are only part of the conditions demanded by Eurozone governments, as there are a whole series of legislative changes demanded in the programme. In the financial sector, it is reiterated that legislation which affects banks will first have to be agreed with the European Commission, European Central Bank, IMF and ESM. And despite the huge amounts of money the Greek government has borrowed to bail out its banks over the last seven years, the Eurozone is demanding that those banks are re-privatised in the ‘medium term’.

The Eurozone governments are also demanding that labour laws are reviewed, including collective dismissal, industrial action and collective bargaining laws, to bring them into line with ‘best practises’ internationally and in Europe. Presumably by ‘best practise’ they mean bring them in line with the most restrictive on the actions of trade unions of any country internationally and in Europe.

The Eurozone governments are also demanding the removal of any restrictions on Sunday trading.

Fourthly, and perhaps most provocatively, there is the demand to sell off up to €50 billion of Greek assets. The demand to sell off certain industries and assets by a given date, leaving the Greek government with little room to bargain, as potential buyers know it is being forced to sell, a true fire sale. Nowhere in the Eurozone demands do they consider whether industries targeted are best run in the public or private sector, nor do they take account of the fall in Greek government income from no longer owning profitable enterprises.

First up is the demand to privatise the ports of Piraeus and Thessaloniki. Piraeus Port is being sold to Chinese company Cosco. The bid deadline for Thessaloniki port is now set for the end of March 2016. Companies interested include Denmark’s APM Terminals and Russia’s state railway company.

The 14 regional airports are being leased to Germany’s Fraport for 40 years for €1.2 billion plus rental fees of €23 million a year. The privatisation of Greek railways and rolling stock has had abid deadline extended to April 2016. Germany’s Siemens and France’s Alstom are said to be two bidders.

The Eurozone governments are demanding Greece privatise the electricity transmission company, ADMIE. The Greek government is still resisting this and trying to find alternative ways to ‘increase competition’ acceptable to the Eurozone.

Eurozone governments state that proceeds from privatisation should be €1.4 billion in 2015, €3.7 billion in 2016 and €1.3 billion in 2017. No mention is made of how much annual government income will be lost from selling off companies which currently bring in revenue.

A condition of the latest loans is also to identify other assets which could be sold, particularly focussing on real estate. The ultimate aim is to raise €50 billion from the privatisation programme, of which €25 billion will be used to repay loans for recapitalising the banks, €12.5 billion for other debt repayments and €12.5 billion for public investments. However, the European Commission estimates that receipts from privatisation will be €13.9 billion by 2022, and doesn’t specify where it expects the further €36.1 billion to come from.

The revenue from privatisations will be put in a fund supervised by ‘the relevant European Institutions’. Just as the Eurozone and EU have demanded privatisation from Greece, they will also decide how the proceeds are spent. As mentioned above, the broad categories have already been decided: three-quarters will be used for debt payments, leaving just one quarter of public investments, decided by ‘European institutions’. Little wonder, then, that even the Financial Times has called the programme ‘akin to the relationship between a colonial overlord and its vassal’.

6. Conclusion

Since 2010 when negotiations over the Greek bail-outs began, developing countries and debt campaigners warned that austerity would crash the economy, increase poverty and unemployment, and increase the relative size of the debt. This is exactly what happened.

The lesson from the debt crisis in developing countries in the 1980s and 1990s is that imposing austerity and refusing to offer significant debt cancellation could drag Greece’s crisis on indefinitely. Yet European decision-makers have ignored these inconvenient truths, and lessons from Greece’s own experience, and dished out a third portion of austerity medicine that will undoubtedly further ensnare Greece in the debt-austerity trap.

Meanwhile, the Eurozone’s paltry proposals for so-called ‘debt relief’’, extending the duration over which the debt is to be repaid, would have no impact on Greece’s debt payments until the 2030s, and pale in comparison to the relief provided by European countries including Greece to Germany after the Second World War. Eurozone proposals would limit Greece’s payments to around 37% of government revenue and 33% of exports, higher than virtually any country in the world today. This is ten times more than Germany’s debt payments following the debt cancellation it received in 1953.

The Third Memorandum also continues to guarantee profits to the IMF, the ECB, and the vulture funds that bought up Greek debts at the height of the crisis, and at the same time forces through further profound and highly regressive and short-sighted restructuring of the Greek economy, with extensive shrinking of the public sector and the welfare state, and a fire-sale of Greek public assets.

The definition of insanity according to Einstein is to keep doing the same thing over and over again with the expectation of different results. From this perspective, the Third Memorandum looks either like act of deluded naivety on the part of the Eurozone and IMF, or a deliberate attempt to keep the Greek economy in recession and stagnation in order to undermine Greece’s sovereignty and maintain influence over its social and economic policies.

Without proper debt cancellation and a reversal of the damaging austerity policies, the people of Greece face many more years and even decades of stagnation, high unemployment, high poverty and increasing debt. A significant write-off of Greece’s debt is the only way to end the never-ending austerity story and give Greece a chance to rebuild its economy and society in the interests of Greece and Europe as a whole.

View and print as a PDF >>

Notes

[1] 36 countries, mainly in sub-Saharan Africa, had $130 billion of debt cancelled in the 2000s.

[2] Argentina in 2002 and Ecuador in 2008

[3] In July 2010, a ‘stress test’ of EU banks was undertaken by the OECD to assess the banks’ exposure to risky assets, including Greek government debt. The analysis showed that banks in eight European countries held €50 billion of Greek government debt. Of the banks in these eight countries, banks in the UK had the fifth largest holdings of Greek debts, after the German, French, Cypriot and Belgian banks. Banks in the UK were identified to be holding €4.1 billion of Greek debt, including RBS, HSBC and Barclays.

[4] The European Stability Mechanism borrows the money on financial markets which it then lends. This borrowing is guaranteed by Eurozone governments, and so ultimately if the ESM were not repaid, Eurozone governments would be responsible for repaying the debt.

Jubilee Debt Campaign

Δεν υπάρχουν σχόλια:

Δημοσίευση σχολίου